Make your investment successful with our local expert

Our firm delivers fast, precise, and reliable advice on investments and deals between Vietnam and Germany, enabling you to grow your business with confidence and efficiency.

Our Expert

Hau Pham

Hau possesses extensive expertise in business deals, partnerships, contracts, and cross-border business expansion between Vietnam and Germany. With a strong background in M&A, partnerships, commercial negotiations, and the Vietnamese legal landscape, she helps clients achieve results promptly and efficiently.

Connect with Hau to experience dedicated service, hands-on expertise, and practical, actionable advice for your business.

Email: hau@onpointbyhau.com

Mobile and WhatsApp:

+49 151 6502 4499

Zalo: +84 908 846 500

Address: In der Clamm 36, 68766 Hockenheim, Germany

MEET HAU PHAM, THE CONSULTANT

Empowering Vietnam–Germany Business Success through OnPoint Consulting

As founder of OnPoint Consulting, I enable German and Vietnamese businesses to succeed in both markets by leveraging my background in Vietnam and my extensive professional experience in Germany. My career began in 2012 as a commercial and M&A lawyer with top international and regional firms, including Allen & Overy (now A&O Shearman) and Rajah & Tann. In 2020, after relocating to Germany and shifting from legal practice to strategy and business management, I developed a broader, commercially focused perspective.

With a Master’s in EU Business Law from the University of Mannheim, I advanced to Strategic Sales Project Manager at ProMinent GmbH, supporting global sales and partnership expansion in industrial water treatment. Since 2023, I join AUMOVIO (formerly Continental Automotive), a DAX-listed leader in autonomous mobility and advanced vehicle technologies, as Partnership Contract Manager.

My experience in Germany’s corporate environment taught me that sustainable business success extends beyond regulations and contracts; it hinges on effective sales, strong partnerships, and profitability. This cross-market expertise enables me to bridge business opportunities between Vietnam and Germany, empowering small businesses to expand confidently across borders.

Through OnPoint Consulting, I advise German and Vietnamese clients on strategy, partnerships, and cross-border operations, underpinned by robust networks in both countries. My consulting practice operates at the intersection of law, business strategy, and international trade.

I am dedicated to structuring and driving deals, supporting market expansion, and enabling partnerships that deliver measurable results. Having championed foreign investment and international cooperation throughout my career, I take pride in helping strengthen trade and investment ties between Vietnam and Germany. For clients seeking flexibility, quality, and results, OnPoint Consulting offers top quality, dedication and precise execution.

Let’s discuss your project!

On a personal note, I am 35 years old. Outside of work, I am a marathon runner and an artisan baker. I enjoy bringing people and ideas together to foster business success.

Vietnam Market Update for German businesses

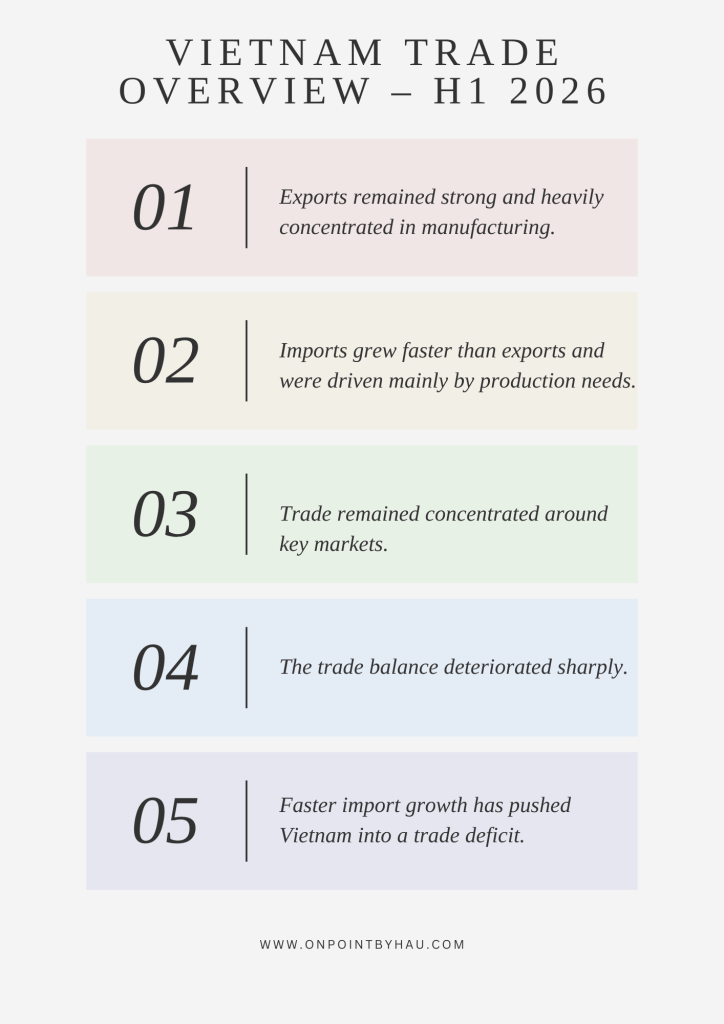

VIETNAM TRADE OVERVIEW – H1 2026

15 July 2026

Vietnam’s external trade remained a bright spot in the first half of 2026, but the structure of that growth deserves close attention from investors.

Total import-export turnover reached USD 549.69 billion in H1 2026, up 27.1% year on year. Merchandise exports totaled USD 266.52 billion, up 21.0%, while merchandise imports reached USD 283.17 billion, up 33.4%. As a result, Vietnam recorded a merchandise trade deficit of USD 16.65 billion, compared with a trade surplus of USD 7.95 billion in the same period last year.

👉 Several points stand out.

1️⃣ Exports remained strong and heavily concentrated in manufacturing.

Processed and manufactured industrial products reached USD 239.8 billion, accounting for 90.0% of total export turnover. The foreign-invested sector, including crude oil, generated USD 213.01 billion, or 79.9% of total exports, while the domestic sector accounted for 20.1%.

2️⃣ Imports grew faster than exports and were driven mainly by production needs.

Import growth was led by machinery, equipment, components, and production materials. Imports of means of production reached USD 266.4 billion, accounting for 94.1% of total imports. Within this, machinery, equipment, tools, and spare parts accounted for 56.0%, while raw materials and fuels represented 38.1%. The Ministry of Industry and Trade (MOIT) stated that this reflected expanding investment and production capacity among enterprises.

3️⃣ Trade remained concentrated around key markets.

The United States remained Vietnam’s largest export market, with export turnover of USD 86.5 billion. Vietnam’s trade surplus with the US reached USD 75.3 billion, up 21.3% year on year. China remained Vietnam’s largest import market, with imports of USD 115.2 billion. Vietnam’s trade deficit with China reached USD 77.3 billion, up 39.0%.

4️⃣ The trade balance deteriorated sharply.

Vietnam recorded a USD 2.64 billion merchandise trade deficit in June 2026. For the first six months of the year, the domestic economic sector posted a USD 24.95 billion trade deficit, while the foreign-invested sector, including crude oil, recorded a USD 8.3 billion trade surplus.

✅ For foreign investors, the practical takeaway is straightforward:

Trade growth remains strong and manufacturing-led, but faster import growth has pushed Vietnam into an overall merchandise trade deficit in H1 2026, while trade remained highly concentrated around the US and China..

Original source: Ministry of Industry and Trade (Q2 / H1 2026 press briefing)

ACCESS TO VIETNAM MARKET FOR FOREIGN INVESTORS

05 July 2026

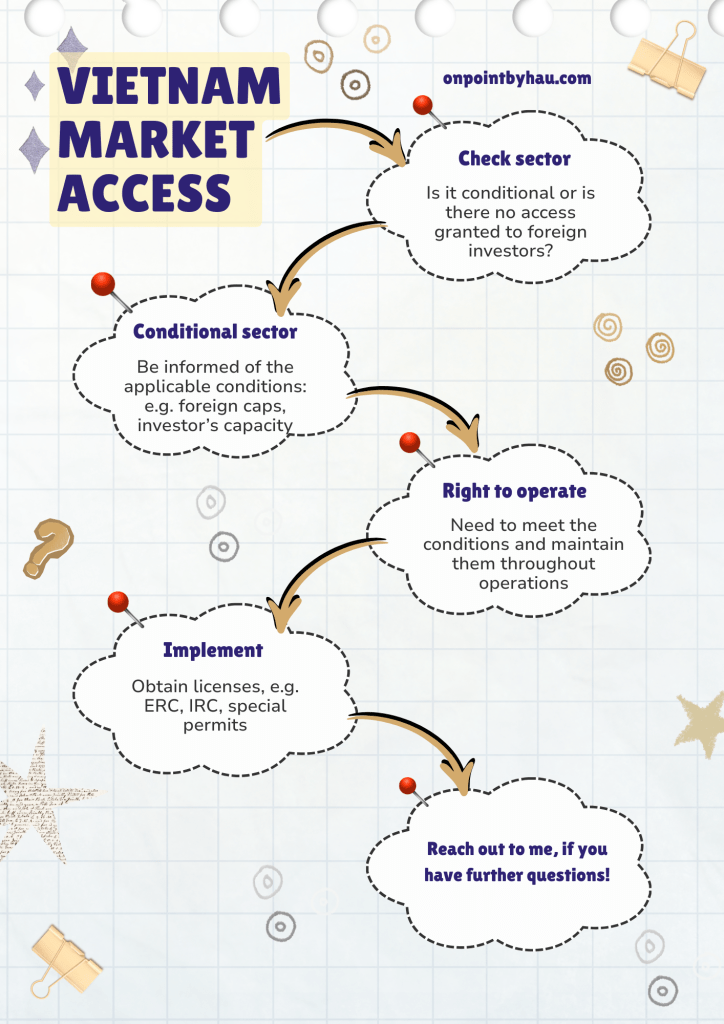

If you are looking at Vietnam, don’t start the first investment question with “What incentive can I get?”

👉 Ask this: Do I have market access for my planned business at all, and on what terms?

This point is still often underestimated by foreign investors looking at Vietnam.

We talk a lot about tax incentives, industrial zones, economic zones, and strategic sectors. Those topics matter. But before that, Vietnam’s Law on Investment and Decree 96 set a more basic gatekeeper: foreign investors are not free to invest in anything they like, in any structure they like.

✅ The law is clear on three points for foreign investors.

1️⃣ Vietnam distinguishes between:

- sectors where foreign investors do not have market access, and

- sectors where foreign investors have market access subject to conditions.

Those conditions can be very practical and commercially decisive. They may include:

🔎 foreign ownership caps, which may require a joint venture with a local partner

🔎 required investment form, for example establishing a company or acquiring equity in an existing company

🔎 limits on the scope of business activities

🔎 conditions on the investor’s capacity, for example an existing licence in its home jurisdiction with a minimum operating history

🔎 conditions on the local partner involved, for example a local partner holding the relevant licence in the relevant field, and

🔎 other requirements under Vietnamese law or applicable international treaties.

Some common examples of conditional business lines include education services and logistics services.

2️⃣ for conditional business lines, the investor only has the right to operate once the legal conditions are fully satisfied. Those conditions must then continue to be maintained throughout the business operation.

3️⃣ a foreign investor may establish an economic organization for an investment project before completing the Investment Registration Certificate (IRC) process. But when doing so, it must still satisfy the market access conditions applicable to foreign investors.

Vietnam is open to foreign investment. But it is not an open field without gates.

✅ So for any foreign investor looking at Vietnam, start here: What is the access route into your sector, and what conditions come with it?

Because in Vietnam, incentives may improve the economics of a project.

But market access determines whether the project can happen in the first place, and how it needs to be structured.

VIETNAM’s LATEST NATIONAL CONFERENCE ON RESOLUTION 10 (FDI GROWTH)

01 July 2026

Vietnam’s latest national conference on Resolution 10 (FDI growth) was less about promotion and more about Vietnam’s self-diagnosis. That is the short investor takeaway.

The Government’s 30 June conference on implementing Resolution 10 suggests that Vietnam’s leadership now sees the old FDI model as insufficient for the next stage of competition. The message was not that foreign capital is less welcome. The message was that capital alone is no longer the benchmark of success.

✅ Three implications stand out.

1️⃣ Vietnam is reframing the competitive proposition.

Ho Chi Minh City’s intervention was unusually clear: the traditional formula of labour, land, and standard tax incentives has reached its limit. Vietnam now wants to compete on institutional quality, capital-market depth, talent, innovation, and asset protection. For investors, that is an important shift in official self-assessment. It means the policy debate is moving from cost arbitrage to ecosystem competitiveness.

2️⃣ The IFC and FTZ agenda should be read as investment infrastructure, not political branding.

The discussion around the International Financial Centre in Ho Chi Minh City and the Free Trade Zone (FTZ) in Da Nang was not presented as symbolic nation-branding. It was framed as part of the machinery needed to attract the next layer of foreign investment: long-term capital, international financial intermediation, logistics depth, digital trade, and higher-value regional functions. Investors should read this as Vietnam trying to strengthen the enabling platform around FDI, not only the front-end pitch.

3️⃣ The real policy shift is from input incentives to output expectations.

The closing agenda from General Secretary Tô Lâm pointed in one direction: less reliance on broad-based input support, and more emphasis on measurable outcomes — domestic supplier linkages, technology spillover, talent development, infrastructure, and better matching between FDI and national strategic priorities. That is more demanding for investors, but it is also more serious. It implies that Vietnam wants the next phase of FDI judged less by volume and more by what the investment changes inside the economy.

👉 What investors should take from this now?

The conference does not mean Vietnam has solved the harder issues. It means the leadership is now naming them more openly.

For foreign investors, the practical takeaway is this:

👉 Vietnam is no longer selling itself only as a location. It is trying to sell a platform.

🤔 The next test will be whether implementation and effectiveness of what will be done by the Vietnamese Government can match the ambition.

Can permitting, infrastructure, skills, supplier depth, and institutional coordination move fast enough to support the direction now being stated at the centre?

That is the question worth watching.

GERMAN COMPANIES ARE TAKING CONCRETE STEPS INTO VIETNAM.

17 April 2026

Germany is not yet one of the largest foreign investor groups in Vietnam. But German businesses are clearly present — and they are making repeated investment decisions.

In Q1 2026 alone (Source: Vietnam FDI Q1 2026 Report):

• 12 new German projects were recorded in Vietnam,

• 10 capital contribution / share-purchase transactions were recorded,

• registered German investment reached around USD 30.2 million, up from around USD 11.3 million in Q1 2025.

As of 31 March 2026, Germany had 523 valid projects in Vietnam, with cumulative registered investment of around USD 3.01 billion.

Vietnam brings together several factors that are hard to ignore: cost competitiveness, industrial capability, growth, and strong trade connectivity.

From a German perspective, the EU-Vietnam trade framework adds another important layer. In practical terms, the EU will progressively remove import duties on goods from Vietnam by 2027.

For companies looking at Asia, the question is often no longer whether Vietnam matters. The real question is how to enter the market in a structured and commercially sensible way.

That is exactly the kind of work I focus on. If your business is looking at Vietnam, I would be glad to exchange views.

Message me, if you like to see the full Q1 2026 report and the data covering investment from 154 countries into Vietnam (in English).

VIETNAM’S INTERNATIONAL FINANCIAL CENTER (IFC): INVESTMENT OPPORTUNITIES TO WATCH

25 March 2026

Content is provided for general informational purposes only and does not constitute legal, tax, accounting, or investment advice. It does not take into account any individual circumstances. Readers should obtain advice from qualified professional advisers before making any business, legal, or tax decisions.

Vietnam has established an International Financial Center under a “one center, two destinations” model with hubs in Ho Chi Minh City and Da Nang, supported by Resolution 222/2025/QH15 and follow-on decrees, including a dedicated decree on IFC tax policy.

Where the opportunities are concentrating

• Capital markets, banking, and fund/asset management (HCMC hub): fundraising, investment banking, payment services, issuance/trading of financial products, and cross-border capital connectivity—areas explicitly positioned as the HCMC hub’s core.

• Fintech + digital finance (Da Nang hub): Vietnam is positioning Da Nang as an innovation-led hub with regulatory sandboxes in digital assets, digital payment services, and specialized trading platforms.

• Market infrastructure builds (institutional “picks-and-shovels”): infrastructure for custody, depository, clearing & settlement, plus digital infrastructure and cross-border payment connectivity—areas flagged as priority investment fields.

• Derivatives and tokenization-linked market deepening: international derivatives (equity/index derivatives) and R&D for asset tokenization and stablecoins are listed within the IFC’s prioritized business scope—high potential if/when implementing rules enable scaling.

• Trade finance and infrastructure funding channels: global institutions have highlighted opportunities in trade finance, corporate treasury services, and support for government bond issuance to fund infrastructure.

• Green finance and energy transition capital: investors are explicitly pointing to Vietnam’s potential in energy transition/renewables, alongside calls for stronger transparency and policy disclosure to improve market liquidity.

• Investor protection and dispute resolution upgrade: a specialized VIFC Court and VIFC Arbitration Center are designed to make high-value cross-border investing more enforceable.

Why investors should pay attention

• Regulatory “special regime”: VIFC rules may prevail over other Vietnamese laws on the same issues (except the Constitution), enabling faster policy adaptation for new financial products.

VIFC tax policy offers significant incentives, including a 10% Corporate Income Tax (CIT) for 30 years for priority industries (4 years exempt, 9 years at 50% reduction) and 15% CIT for 15 years for other industries. Personal Income Tax (PIT) is exempt for key talent until 2030.

• Dispute resolution upgrade: a dedicated VIFC Court plus a VIFC Arbitration Center.

• Cross-border flexibility: the framework contemplates greater ease for IFC members to transact with offshore investors and access offshore funding, subject to implementing rules.

Other key policies

• Visa/Residency: 10-year visas and temporary residence cards are available for eligible investors/experts/managers and their families.

• Accounting: IFC members may use International Accounting Standards (IAS) or other international GAAP rather than Vietnamese Accounting Standards (VAS).

• Foreign Exchange: Relaxed regulations for capital transfers and transactions in foreign currencies for transactions among IFC members and/or offshore counterparties.

Our observations

VIFC is architecturally closest to DIFC (Dubai International Financial Centre)/ADGM (Abu Dhabi Global Market) (financial free-zone model with dedicated legal/regulatory infrastructure), and also comparable to QFC (Qatar Financial Centre)/AIFC (Astana International Financial Centre) as “special regimes” designed to reduce cross-border friction via dedicated rules and dispute resolution.

VIETNAM WAS ADDED TO THE EU LIST OF NON-COOPERATIVE JURISDICTIONS FOR TAX PURPOSES

24 February 2026

Content is provided for general informational purposes only and does not constitute legal, tax, accounting, or investment advice. It does not take into account any individual circumstances. Readers should obtain advice from qualified professional advisers before making any business, legal, or tax decisions.

Update based on EU Council’s press release regarding EU list of non-cooperative jurisdictions for tax purposes

On 17 February 2026, the Council adopted the EU list of non-cooperative jurisdictions for tax purposes. Vietnam is one of the 10 countries on the list. To be considered cooperative for tax purposes, jurisdictions are screened on a number of criteria, established by the Council. The listing criteria relate to: tax transparency, fair taxation and measures against base erosion and profit shifting (‘anti-BEPS measures’).

Viet Nam was included in the EU list after the OECD Global Forum’s review revealed that the country did not meet the necessary standards for the exchange of tax information on request.

Since it was first established in 2017, the list has been updated regularly and revised as a result of dynamic monitoring of the measures implemented by jurisdictions to comply with their commitments. The list is to be updated twice a year. The latest revision took place in February 2026. The next revision is due in October 2026.

The Council announced that their aim with this list is to encourage positive change in their tax legislation and practices through cooperation. Once a jurisdiction meets all its commitments, its name is removed from the list.

In principle, the EU cannot and does not impose taxes on citizens or companies. For the EU list to be effective, it is important that EU member states put in place efficient defensive measures in non-tax and tax areas. Defensive measures help to protect EU member states’ tax revenues and fight against tax fraud, evasion and abuse. EU member states have broad discretion over the type and scope of defensive measures they apply in the tax area. These largely depend on their national tax systems. Nevertheless, there is a certain degree of coordination within the EU.

Observations (Germany-focused, indicative only):

For German groups with operations in Vietnam, the EU listing may lead to increased tax and compliance scrutiny and—depending on German implementation and effective dates under Germany’s defensive tax framework (e.g., the Tax Haven Defence rules)—potential measures such as stricter CFC / Hinzurechnungsbesteuerung for certain low-taxed subsidiary income, expanded withholding tax obligations for specific payment types, limitations affecting participation exemptions on dividends/capital gains, and restrictions on deductibility of certain expenses. The applicability, scope, and timing depend on the specific facts, payment streams, and the relevant German rules in force at the time.

VIETNAM ACCEDES TO THE HAGUE APOSTILLE CONVENTION (1961) – POTENTIAL ADMINISTRATIVE EFFICIENCY IN CROSS-BORDER TRANSACTIONS

15 February 2026

Vietnam has acceded to the Hague Apostille Convention, a development expected to enhance cross-border administrative efficiency for businesses and individuals. Germany is currently a member to the Hague Apostille Convention (1961).

Once in force, the Convention will replace the consular legalization step for qualifying public documents exchanged between Vietnam and other Convention member states. Instead of multi-layer authentication involving embassies or consulates, a single Apostille certificate issued by a designated competent authority will be sufficient.

Practical implications:

(i) Reduced procedural steps in cross-border documentation,

(ii) Shorter processing timelines, and

(iii) Lower authentication-related administrative costs.

This is particularly relevant for corporate documents, powers of attorney, commercial registrations, and certain personal status documents used in international investment, M&A, and regulatory filings.

Timing and implementation:

The Convention will take effect between Vietnam and other member states that do not object to Vietnam’s accession as of 11 September 2026. Vietnam has designated the Ministry of Foreign Affairs as the competent authority to issue Apostille certificates, including: the Consular Department (headquartered in Hanoi) and the Ho Chi Minh City Department of External Relations (Cục Lãnh sự (trụ sở tại Hà Nội) và Sở Ngoại vụ thành phố Hồ Chí Minh). However, detailed domestic implementation is still expected. Practical application will depend on these implementing measures.

Further updates will follow once Vietnam issues more concrete regulatory guidance clarifying scope, procedures, and operational details.

REGULATORY & TAX CHANGES AFFECTING FOREIGN SMES IN VIETNAM

02 Jan 2026

Vietnam remains attractive for German SMEs, but the regulatory and tax environment has become noticeably stricter. Authorities have tightened rules on transfer pricing and related-party transactions, lowering tolerance for informal intercompany arrangements and incomplete documentation. This shift is no longer limited to large multinationals—foreign-invested SMEs are increasingly subject to tax audits, particularly in areas such as service fees, management charges, and profit allocation.

At the same time, companies face closer scrutiny on VAT refunds, withholding tax, and permanent establishment (PE) risks. German firms providing services remotely or through short-term personnel in Vietnam are more frequently challenged on whether their activities trigger local tax obligations. Parallel to this, Vietnam’s tax administration is rapidly digitalizing, with mandatory e-invoicing and enhanced data cross-checking significantly increasing transparency and audit efficiency.

Bottom line for German SMEs: Vietnam is still business-friendly, but compliance expectations have risen sharply. Early investment in proper accounting, robust contracts, and defensible intercompany pricing is no longer optional—it is essential to control risk and avoid costly disputes later.

VIETNAM’S ROLE IN SUPPLY CHAIN DIVERSIFICATION FOR THE GERMAN MITTELSTAND

02 Jan 2026

Vietnam continues to strengthen its position as a key manufacturing and sourcing hub for German SMEs as part of China+N strategies. Competitive labor costs, tarade agreements, and a growing supplier base make Vietnam attractive for electronics, machinery components, textiles, and consumer goods.

However, SMEs face practical constraints: shortages of skilled labor, infrastructure pressure in industrial zones, and uneven compliance standards among local suppliers. In addition, legal and tax risks in contract manufacturing, OEM/ODM models, and tooling ownership are often underestimated and can lead to loss of IP or unexpected tax exposure. ESG and supply-chain due diligence expectations from Germany are also rising and increasingly enforced through customer audits.

Key takeaway: Vietnam offers real opportunities, but success now depends on strong supplier governance, clear contracts, and disciplined risk management, not cost arbitrage alone.

German Market Update for Vietnamese businesses

GERMANY COFFEE MARKET FOR VIETNAMESE PRODUCERS

1 Feb 2026

- Market Size & Importance

Germany is the largest coffee market in Europe and one of the top global hubs for coffee trade and processing.

According to Deutscher Kaffeeverband (German Coffee Association), Germany imports ~1.2–1.3 million tonnes of coffee per year (mostly green coffee).

Average amount consumed per person: ~163 liters/year, among the highest globally.

Global context:

Largest coffee consumer by volume: USA, Germany ranks top 5 worldwide and #1 in Europe (source: Deutscher Kaffeeverband, ICO).

- Where Germany Imports Coffee from

According to Deutscher Kaffeeverband (using Destatis/Eurostat trade data):

Ranking based on Country Share of Importation:

1 – Brazil ~40% Arabica-dominated, price anchor

2 – Vietnam ~15–16% Robusta leader

3–5 Honduras, Colombia, Uganda ~4–6% each Arabica / specialty / Robusta

➡️ Vietnam is already Germany’s #2 supplier, but mainly positioned as volume Robusta

- Form of Coffee Imported into Germany

According to Deutscher Kaffeeverband (using Destatis/Eurostat trade data), 95% of imports are green (raw) coffee beans.

After green coffee arrives (mostly via Hamburg, Europe’s largest coffee port), the German supply chain will handle storage & trading (commodity traders, houses), roasting (industrial + specialty roasters), further processing like: ground coffee, Capsules / pads and instant coffee, then re-export across Europe.

➡️ A large share of coffee imported into Germany is processed and then exported again.

For Vietnamese exporters:

Germany is not just a buyer, but a gateway to Europe.

Vietnam already plays a critical role—but future growth depends on moving from volume-only Robusta to reliability, certification, and partnership-driven supply.

Consider: Direct trade models and Long-term supply contracts (risk-sharing)

Target business: German roasters (private label, B2B) and Importers serving EU-wide distribution

Key sources: Deutscher Kaffeeverband (German Coffee Association), Destatis (German Federal Statistical Office), International Coffee Organization (ICO)

COMMON COMPANY & BUSINESS FORMS FOR FOREIGN INVESTORS ENTERING GERMANY

4 Jan 2026

Disclaimer: This overview is provided for general information purposes only and does not constitute legal, tax, or investment advice. It does not take into account individual circumstances, and no liability is assumed. Professional advice should be obtained before making any business or investment decisions.

Choosing the right legal form depends on capital availability, risk exposure, speed of entry, and long-term business objectives. Below is an overview of the most common and practical options for foreign investors, not to aim to provide a list of all available forms (some of which are OHG, Kommanditgesellschaft and GmbH & Co. KG).

GmbH (Gesellschaft mit beschränkter Haftung)

Best for: serious, long-term market entry

• Pros: Limited liability; strong credibility with banks, customers, and authorities; flexible shareholder structure

• Cons: €25,000 share capital (minimum €12,500 payable upon formation); higher setup and ongoing compliance costs

• Typical use: Operating businesses, manufacturing, sales, and services

• Indicative timeline: ~4–8 weeks (depending on banking and notarization)

The GmbH is widely regarded as the standard and most defensible structure for foreign investors.

UG (haftungsbeschränkt) – “Mini-GmbH”

Best for: early-stage market testing or pilot projects

• Pros: Limited liability; can be formed with very low share capital (from €1 in theory)

• Cons: Lower market credibility; mandatory retention of 25% of annual profits until €25,000 share capital is reached

• Typical use: Pilot projects, startups, initial market entry

• Indicative timeline: ~3–6 weeks

In practice, higher initial capital is usually required for banking and operational reasons. The UG is generally considered a temporary structure, often with a planned conversion into a GmbH.

Branch Office (Zweigniederlassung)

Best for: foreign companies seeking direct operational presence without forming a subsidiary

• Pros: No share capital requirement; direct integration into the parent company

• Cons: Parent company is liable with all its global assets, not only German assets;

• Typical use: Sales or service extensions of an existing foreign company

• Indicative timeline: ~4–6 weeks

A branch office must be registered and may conduct business in Germany. The unlimited parent liability is often a key decision factor for foreign boards.

Bottom line

• GmbH: Best balance of credibility, flexibility, and risk protection

• UG: Low-cost entry for testing the market, with structural limitations

• Branch Office: Faster entry, but significantly higher liability and tax exposure (not a common choice)

For most foreign investors planning to operate in Germany, GmbH or UG are the most practical and defensible choices.

Is there something like a “Representative Office”?

German law does not recognize a representative office as a formal legal entity. The term “Representative Office” is an informal business practice, not a statutory company form.

In practice, it is usually implemented as:

• A non-commercial presence

• Activities strictly limited to market research and liaison functions

• Pros: Low cost; minimal setup

• Cons: No commercial activity allowed; no revenue generation; not registrable in the Commercial Register (Handelsregister)

Note on other business forms

Germany also offers other structures such as partnerships, joint ventures, and corporate forms like AG or SE. These may be relevant in specific scenarios but are not suitable for most small businesses or companies in an early exploration phase.